Lingye

Lingye

Everyone wants to own NVIDIA. Almost nobody stops to ask who actually makes NVIDIA's chips. The answer is a single company on the other side of the world, and it sits closer to the center of the AI boom than the famous names that get the headlines. If you want to understand AI investing — or own a piece of it — you eventually have to understand TSMC.

I've spent fifteen years investing while living across Asia, an hour's flight from where most of the world's advanced chips are physically made. TSMC is the foundry layer of the chip value chain — the company NVIDIA, Apple and AMD all depend on to turn a design into silicon. This guide is how I think about investing in TSMC in 2026: what it is, why it's the chokepoint of the whole AI trade, how to actually buy it, and the concentration risk nobody puts on the brochure. No price targets.

What TSMC actually is

TSMC — Taiwan Semiconductor Manufacturing Company — invented the "pure-play foundry" model: it doesn't design or sell its own chips, it just manufactures other companies' designs, better than anyone else. It's the largest dedicated chip foundry in the world, with roughly 60–70% of the global foundry market (estimates vary; verify the latest on TSMC's own filings). Centered on Hsinchu, with giant fabs in Tainan and Kaohsiung, it makes the chips inside your phone, your laptop, and nearly every AI accelerator on earth.

The reason it matters for an investor is simple: there is no real alternative at the leading edge. When you buy an advanced chip from anyone, a TSMC fab almost certainly built it. That makes TSMC less a bet on one product and more a toll booth on the entire industry.

Why TSMC is the chokepoint of the AI boom

Designing a chip and manufacturing it are completely different businesses, and the manufacturing has consolidated into one dominant player at the cutting edge. NVIDIA's GPUs, Apple's processors and AMD's accelerators are all fabricated by TSMC. Its newest 2-nanometer process entered volume production around the end of 2025 and is ramping fast in 2026 — and it's effectively booked, with long lead times. When the most advanced capacity in the world is sold out, the company that owns it has pricing power.

There's a second, quieter chokepoint: advanced packaging. The step that bonds high-bandwidth memory to a logic chip — TSMC calls it CoWoS — is where AI accelerators are physically assembled, and that capacity has been sold out too, with TSMC scaling it several-fold through 2026 and one large customer reportedly booking the majority. So TSMC isn't just making the chip; it's also doing the packaging the AI boom can't ship without.

NVIDIA designs the engine, but TSMC builds it. In the AI gold rush, TSMC isn't panning for gold — it owns the only smelter that works at the leading edge.

This is the "Foundry" layer I describe in my map of the AI chip value chain — and it's the layer most retail investors overlook while chasing the design names.

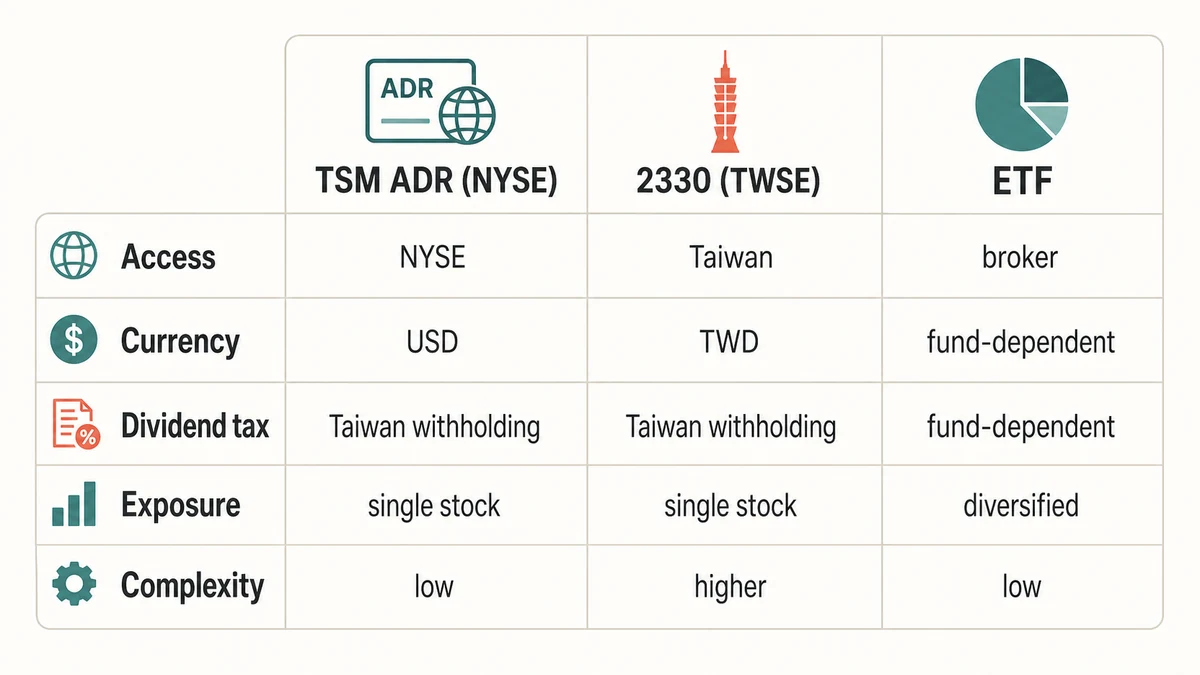

TSM (ADR) vs Taiwan 2330: how to actually buy it

You have two ways to own TSMC, and for most people one is obviously simpler.

| Route | Ticker | What it is | Best for |

|---|---|---|---|

| US-listed ADR | TSM (NYSE) | An American Depositary Receipt — TSMC shares wrapped to trade in US dollars on the NYSE | Almost everyone outside Taiwan |

| Home listing | 2330 (TWSE) | The original shares on the Taiwan Stock Exchange, in New Taiwan dollars | Investors with direct Taiwan-market access |

For a US investor, the ADR (TSM) is the simple answer: you buy it in dollars through any normal US brokerage, exactly like a domestic stock. One detail to know before you buy for income: TSMC pays a cash dividend, but dividends on the ADR are generally subject to a Taiwan withholding tax for foreign holders, which affects your net yield — check the current rate and how your broker handles it.

The bull case, in one idea

Strip away the noise and the case for TSMC is a single sentence: it collects a fee on almost every advanced chip the world makes, and the world is making more of them. AI high-performance computing has become its main growth engine, North America is now the majority of its revenue, and management has guided to strong revenue growth into 2026 on that demand. A near-monopoly at the leading edge, with sold-out capacity and pricing power, is a rare thing to be able to buy.

It's also building beyond its home base — new fabs in Arizona, Kumamoto in Japan, and Dresden in Germany — which both follows its customers and slowly spreads its manufacturing footprint. That global build-out is a real part of the long-term story.

The risks nobody puts on the brochure

A toll booth is wonderful until something threatens the road. TSMC's risks are specific and worth naming honestly:

- Geographic concentration. The large majority of the world's leading-edge capacity sits in one place. Any disruption there — natural or political — is the single biggest risk to the stock, and it's not one a spreadsheet can price.

- Customer concentration. A handful of customers, led by the big AI and phone names, drive a large share of revenue. If their demand wobbles, TSMC feels it.

- Brutal capital intensity. Staying ahead costs tens of billions a year in new fabs and tools. That capex is the moat, but it also means the business is cyclical and sensitive to any slowdown.

- Valuation and the cycle. After a huge run, a lot of optimism can already be in the price. A great company bought at the wrong moment is still a poor entry.

Buy TSMC directly, or own it through an ETF?

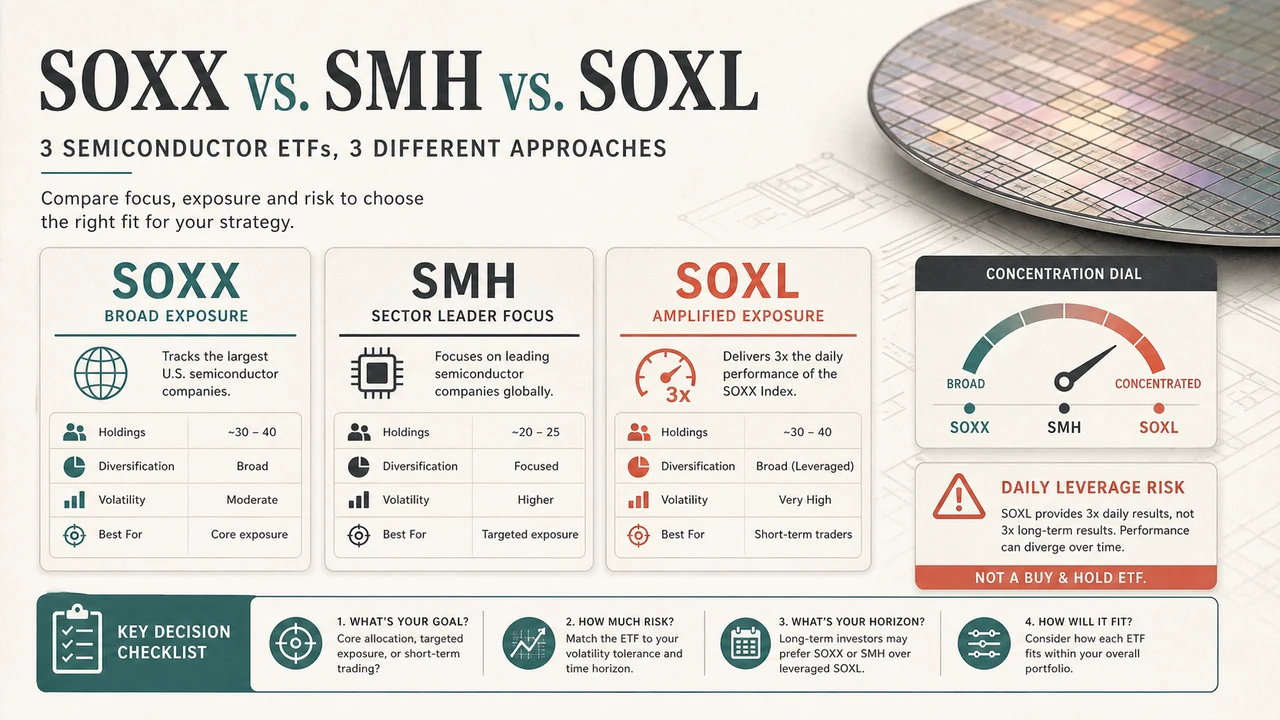

You don't have to choose a single stock to own TSMC. A broad semiconductor ETF holds it for you — and one of the two big funds, VanEck's SMH, typically keeps TSM near the top of its portfolio, which is exactly why I call SMH the more "international" of the chip ETFs. If you'd rather own TSMC as part of a basket than as a concentrated single-name bet, that's the calmer route. I compare the options in my guide to SOXX vs SMH vs SOXL.

A simple way to decide

- Do you want the foundry layer specifically? If yes, TSM (ADR) is the cleanest single-name way to own it.

- Can you stomach single-stock and single-region risk? If that concentration worries you, own TSMC through a semiconductor ETF instead.

- Are you buying for income? Factor in the Taiwan dividend withholding on the ADR before you count the yield.

- Has it just run hard? Excitement isn't an entry signal. Size the position so a bad year is survivable.

This is educational, not personalized financial advice. I'm not a financial advisor, I don't know your situation, and nothing here is a recommendation to buy or sell TSM or any security. Semiconductor stocks are volatile and cyclical, single-stock and single-region concentration is a real risk, and you should verify every figure on primary sources and consider a licensed professional before investing.

Pitfalls I've watched people hit

- Owning NVIDIA and TSMC and a chip ETF and calling it diversified. They overlap heavily — it can be the same AI bet three times.

- Forgetting the dividend withholding. The ADR's headline yield isn't what lands in your account after Taiwan's withholding.

- Treating concentration risk as zero because it hasn't happened. It's a low-probability, high-impact risk — size accordingly rather than ignoring it.

- Chasing after a parabolic run. The best company in the world can still be a bad entry at the wrong price.

FAQ

How do I invest in TSMC from the US?

The simplest route is the US-listed ADR, TSM, on the NYSE — you buy it in US dollars through any standard US brokerage, just like a domestic stock. The alternative is buying the original shares (ticker 2330) on the Taiwan Stock Exchange, which requires direct access to that market and is unnecessary for most investors. Note that dividends on the ADR are generally subject to a Taiwan withholding tax for foreign holders, so confirm the current rate and your broker's handling before buying for income.

Is TSMC a good AI stock?

TSMC is the foundry that manufactures the chips for nearly every major AI company, so it's arguably the most direct way to own the "picks and shovels" of the AI boom rather than a single design. Its leading-edge and advanced-packaging capacity has been effectively sold out, which gives it pricing power. The trade-offs are heavy geographic and customer concentration and a cyclical, capital-intensive business. Whether it fits you depends on your tolerance for those risks — this is educational, not advice.

What is the difference between TSM and 2330?

They're the same company. TSM is the US-listed American Depositary Receipt that trades in US dollars on the NYSE; 2330 is the original ordinary share that trades in New Taiwan dollars on the Taiwan Stock Exchange. For most investors outside Taiwan, the ADR is the practical choice because it's reachable through a normal brokerage. The underlying business is identical, though the ADR carries the dividend-withholding nuance and trades on US hours.

Why is TSMC so important for NVIDIA?

NVIDIA designs its GPUs but doesn't manufacture them — TSMC does, on its most advanced process, and TSMC also does the CoWoS advanced packaging that bonds high-bandwidth memory to the GPU. In practice, NVIDIA's ability to ship is gated by how much leading-edge and packaging capacity TSMC can give it. That's why the two are so tightly linked, and why TSMC's capacity is one of the real bottlenecks of the entire AI hardware cycle.

Does TSMC pay a dividend?

Yes, TSMC pays a regular cash dividend. If you hold the US-listed ADR (TSM), those dividends are generally subject to a Taiwan withholding tax for foreign investors, which reduces the net yield you actually receive compared with the headline figure. The exact rate and the way it's applied can change and depend on your situation, so verify the current treatment and check how your broker processes it before relying on TSMC for income.

The bottom line

TSMC is the closest thing the AI boom has to an indispensable company: the foundry the whole industry runs through, with sold-out leading-edge and packaging capacity and genuine pricing power. The case against it isn't the business — it's concentration, in one region and a few customers, plus a cyclical, capital-hungry model and a price that already reflects a lot of good news. Own it directly through the TSM ADR if you want the foundry layer specifically and can hold the risk; own it through a chip ETF if you'd rather not bet the farm on one name.

For the full picture, read my map of the AI chip value chain, how to read Micron and the memory layer, and the SOXX vs SMH vs SOXL ETF comparison. Browse more in my Smart Money and Asia Markets coverage.